One of the primary ways students receive assistance in paying for college is through federal financial aid. The Department of Education’s Office of Federal Student Aid (FSA) administers all financial aid programs authorized in Title IV of the Higher Education Act (HEA). Title IV of the act created several financial aid programs targeted to students who would not otherwise have the means to afford college. The programs under Title IV include Pell Grants, federal student loans, and Federal Work-Study, among others.

For the 2015-16 school year, about 1,300 community colleges opted to participate in Title IV programs. To opt in, institutions must be authorized to provide postsecondary education by the state where they operate, be accredited by a nationally recognized accrediting body, and admit students who have completed high school or the equivalent or are past the age of mandatory school attendance.

Students must also meet basic requirements to apply for aid. All Title IV programs require recipients to be a United States citizen or eligible non-citizen, have a Social Security Number, and not be in default on any federal student loans, among other criteria. Although these programs are typically for students with demonstrated financial need, students without need often qualify for unsubsidized federal loans. Students must reapply for aid each year and meet institutional standards of academic progress.

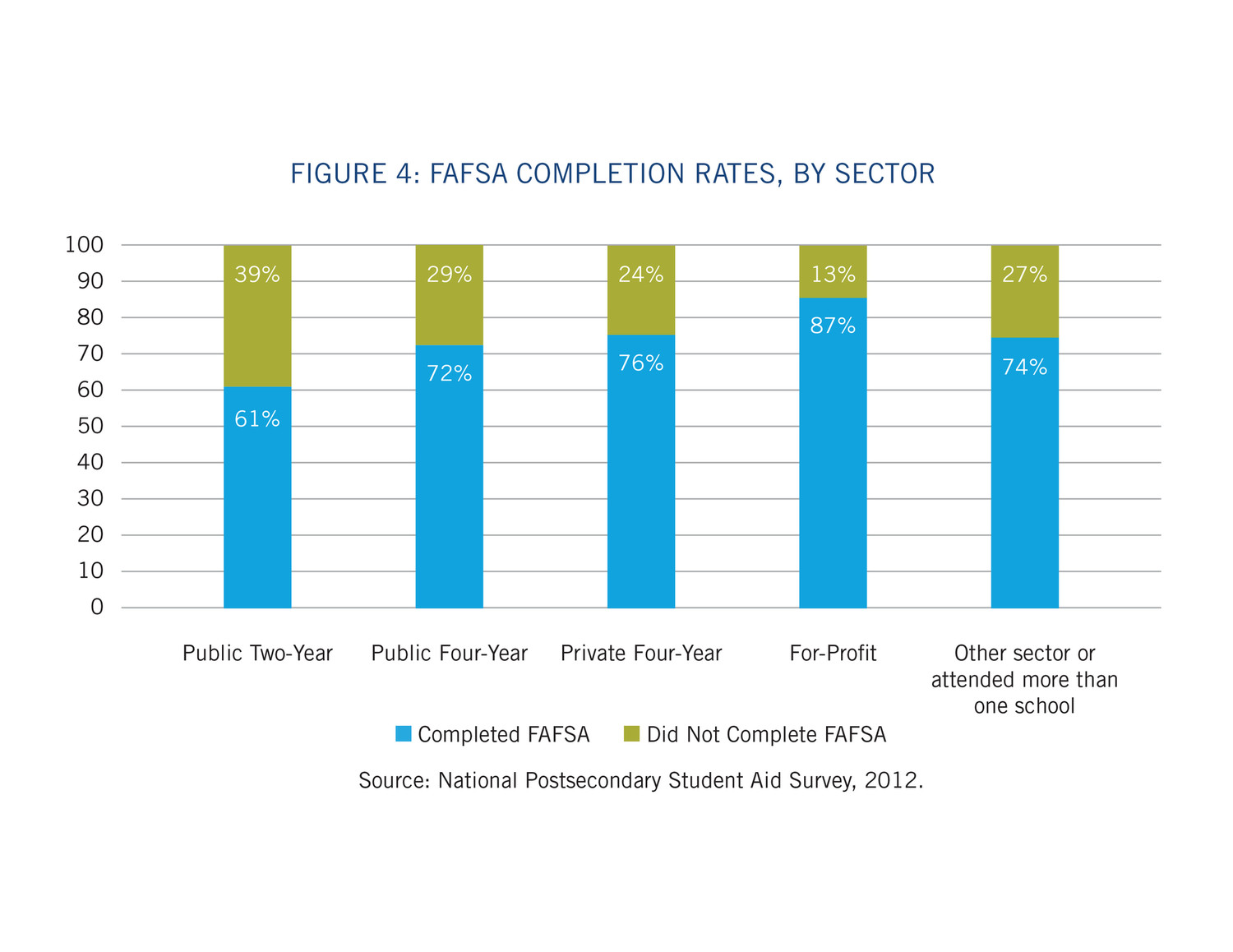

To apply for any federal student aid, students must complete the Free Application for Federal Student Aid (FAFSA) each year to maximize the support they receive. In addition to federal student aid, state and institutional aid eligibility is often based on FAFSA data. Unfortunately, nearly 40% of community college students do not complete the form. Students who fail to file could be leaving thousands of dollars on the table, money that could mean the difference between a degree and dropping out.

The FAFSA is available as an online form at www.fafsa.ed.gov. When a student completes a FAFSA, they receive a figure called the Expected Family Contribution (EFC) which determines their eligibility for federal aid. The FAFSA asks for significant information from students whose families make $25,000 or more per year, but the EFC is heavily determined by the student’s family income, assets and household size.

As of October 1, 2016, FAFSA applicants can use tax data from two years prior, rather than the previous year to complete the form. This allows for reduced delay in receiving financial aid award eligibility. Going forward, the FAFSA will also be available on October 1 of the academic year, as opposed to January 1. These policy changes, respectively known as Prior-Prior-Year and Early FAFSA, offer applicants the ability to use correct, readily available tax information, which in turn allows institutions to provide students with earlier notification of financial aid awards for the following school year.

Financial aid administrators at the student’s institution use the student’s EFC, cost of attendance (including tuition, fees, room, board, books and supplies, transportation, and personal expenses), and federal, state, and institutional aid eligibility requirements to prepare the student’s financial aid package, which is detailed in a financial aid award letter sent to the student.

After students receive their aid letters, they have a few decisions to make. First, students need to see how much money they need to cover their expenses after grants and scholarships have been applied. If they have remaining expenses, they may choose to cover the rest using student loans offered in their financial aid letter or to work to meet their expenses. Students also need to decide if they plan to attend college full-time or part-time. This is an important decision, because the size of awards for some aid programs is contingent on students’ enrollment intensity.

Once students have accepted appropriate aid and enrolled, financial aid administrators can apply student aid to their institutional account. Any aid, including loans, that exceeds the amount payable to the institution will be refunded to the student, usually by check or direct deposit. Per cash management regulations, institutions are required to offer students their choices of several ways to receive their student aid refund. Refunded student aid can be used to meet other living expenses while the student is enrolled in college.

For more information, please see ACCT's Financial Aid 102: An Updated Guide to Understanding Federal Financial Aid Programs for Community College Leaders and Trustees (2017).

Jacob Bray is an associate writer for the Association of Community College Trustees.