In July 2014, Des Moines Area Community College (DMACC) faced a projected FY2013 cohort default rate of 35.6%. “Prior to that time we played the ‘default roulette game’ – wait until the estimated rate was released and then work like heck to identify borrowers to appeal. Not the most practical approach, but the one we had been following for a number of years,“ said Dr. Laurie Wolf, Retired Executive Dean of Student Services.

DMACC recognized that it was missing some vital skills that would be difficult to develop internally, such as skip tracing staff, and made the decision to contract with a third party servicer to address getting the rate under control. With the assistance of staff at EdFinancial Services, DMACC embarked on an aggressive campaign to address the reasons why students default.

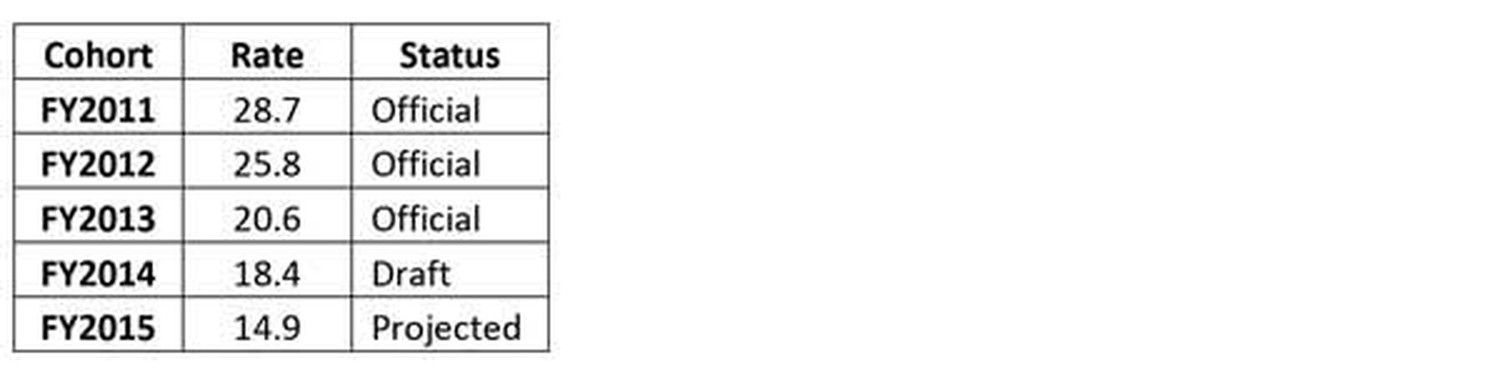

EdFinancial Services staff conducted a two-prong outreach campaign of delinquent borrowers within the FY2013 cohort: (1) pursue all borrowers who were 90+ days delinquent, and (2) work with defaulted borrowers to successfully rehabilitate their loans so they could be excluded from the calculation prior to the official cut date. In addition, EdFinancial Services instructed DMACC staff in how to better analyze NSDLS data and analysis tools available to schools. Through these efforts 96 borrowers were rehabilitated and DMACC achieved a 20.6% official cohort default rate for FY2013. A 15.0% drop from its projected rate and 5.2% down from the FY2012 rate.

In addition to contracting with EdFinancial Services, DMACC staff conducted an analysis of the FY2013 cohort based on the study: Multivariate Analysis of Student Loan Defaulters at Texas A&M, to determine contributing factors of default. Results of DMACC study: 91% of defaulters had no credentials, only 7% achieved an Associate Degree; Student Loan Servicers placed 78.3% of the borrowers in Standard Repayment Plans while only 17.7% were placed in Graduated/Income Contingent Plans; 40% of the defaulters had less than $5,000 in debt; the highest level of borrowing was done by reverse transfers; and borrowers transferring to another institution did not always obtain an in-school deferment. In an unrelated enrollment analysis project, DMACC determined that 60% of the currently enrolled students do not actively update their contact information with the college.

Early in this project the DMACC community embraced the concept that student loan defaults are not isolated to the efforts of the Financial Aid Office. Based on the results and explanation of the data analysis, academic and student services offices were willing to explore what they could do to identify possible contributing factors and how to counter them. These efforts have helped DMACC to see a steady reduction in its rates.

· Instituted Pathways Advising for students during their first semester of enrollment. Through this program students work with their College Experience (SDV108) instructor to develop a two-year completion plan, outlining all courses that need to be completed and a schedule of when those courses should be taken.

· An Early Alert System was implemented which allows faculty and staff to report to the DMACC Advising & Counseling staff when they have observed a student having difficulties. The reporting includes: students in academic difficulty, students missing more than two consecutive class meetings, change in behavior, student who might benefit from tutoring or assistance from the Academic Achievement Center, or students disclosing financial, family or health issues. Advising & Counseling staff report that 58% of the students reported were enrolled in the following semester, compared to 52% who were not identified through the Early Alert System.

· EdFinancial staff counseled severely delinquent borrowers in options to correct their situations. In multiple cases borrowers reported that they had never been told about Income Based Repayment options, or ways to take care of their delinquent amounts, including deferments.

· In addition to working with severely delinquent borrowers, EdFinancial staff also reached out to students with very low loan balances. These borrowers were reminded to keep making their payments and to especially make their last payment.

· When incoming transfer students are identified, Financial Aid and Advising & Counseling staff reach out to them to discuss the amount of their previous borrowing and to discuss their past educational experiences to determine what support services are needed for the students to be academically successful while at DMACC.

· Currently enrolled student borrowers are sent information concerning how to contact their loan servicer to inform the servicer of their in-school status.

· Students who have entered repayment are provided important information regarding how to contact their servicer, and are also given the option to be warm-transferred to their servicer during telephone outreach.

· Students who leave DMACC are sent information reminding them of their student loan debt, their student loan servicer, and how to go about applying for an in-school deferment should they be enrolling at another institution.

· DMACC developed detailed policies regarding fraud prevention and unusual enrollment history to ensure students are accessing federal loans for an educational purpose.

· DMACC introduced a loan disbursement policy for distance education students that encourages participation as recommended by Dear Colleague Letter GEN-11-17.

· At the point of registration for each semester students are asked to confirm their contact information. This assures that DMACC has the most up-to-date contact information when communicating DMACC related information to the students, and also, allows DMACC to provide up-to-date information to NSLDS and to the National Clearinghouse for their tracking and contact purposes.

“Default prevention is not about finding the silver bullet that will single-handedly lead to a successful reduction of an institution’s default rate. It’s about researching the influential factors and addressing them through a multifaceted approach,” states Ean Freels, DMACC Financial Aid Director. “It’s not a special program or tool that Financial Aid Administrators introduce and then subsequently move on to the next fire to put out. It is a way conducting business within the Financial Aid Office that must become as routine as awarding or originating. The policies, procedures, duties, and responsibilities must be introduced into our daily processes”.